Evidence-based environmental-economic policy making

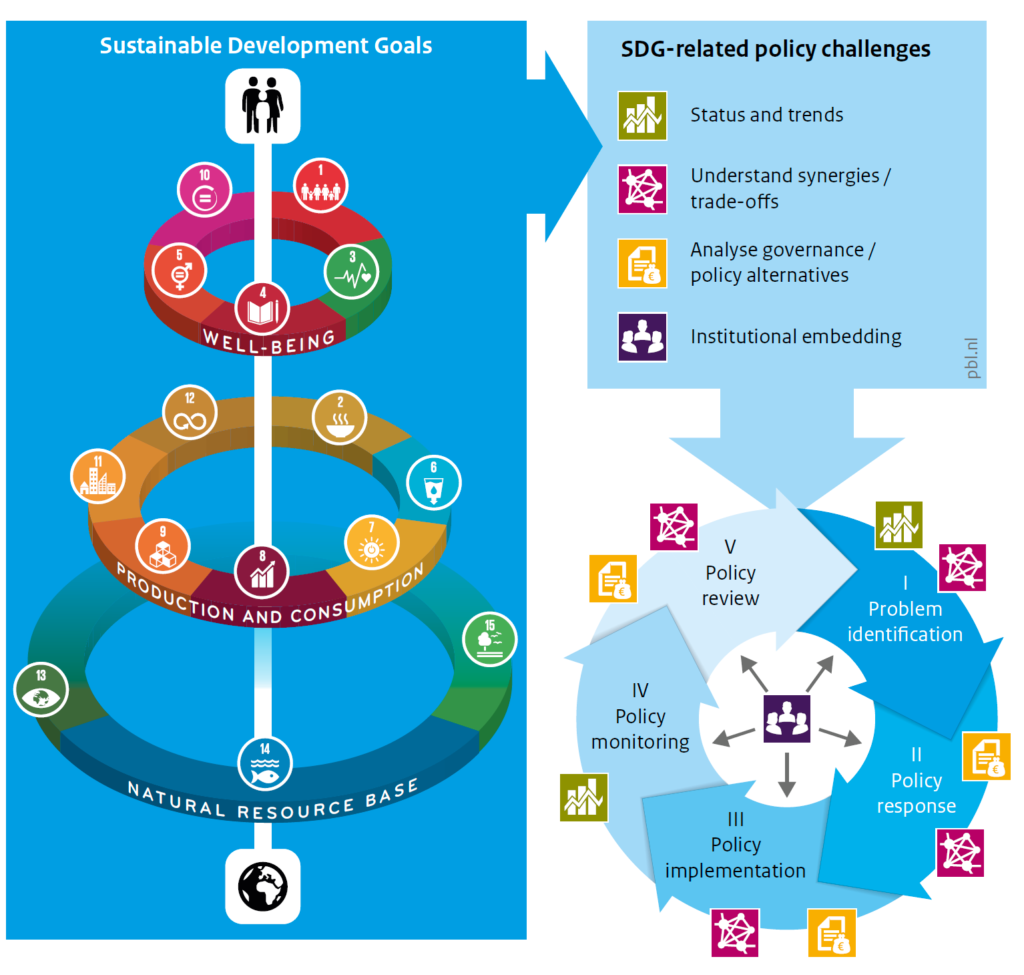

Our society is facing multiple crises such as climate change and increasing biodiversity loss as well as economic instability and social inequality. Environmental pressures and impacts are unintended consequences of current production and consumption systems. While environmental policies aim at conserving natural resources and reducing waste and emissions while increasing well-being and material standards of living, such sustainability policy issues become increasingly complex. This complexity requires concerted policy effort to manage trade-offs and potential interrelations among different environmental and economic areas. To realise a turnaround towards more sustainable consumption and production, action on all social and administrative levels is needed, starting with local and regional action, following national measures and plans that are aligned with global strategies. This approach has been manifested in the UN Sustainable Development Goals (SDGs). The following figure exemplarily shows the interplay between the SDGs, thereout arising challenges and the relevance of these in the policy cycle, highlighting thorough information on environmental and economic issues as a fundamental part of evidence-based policy making.

(Ruijs A. et al., 2018)

Policymakers and executive authorities require a solid data basis, to identify hotspots for policy interventions, monitor outcomes as well as to reconcile and improve policies. In this respect, comparability of data from environmental and socio-economic domains is of high relevance. To align monitoring and policy actions among different actors and administrative levels, a common framework is needed that allows describing the interlinkages between the economy and the environment in a consistent manner.

The UN System of Environmental Economic Accounting (SEEA) was designed to provide this information and constitutes the fundamental standard for capturing interactions between the environment, private households, and the economy. To achieve this, physical environmental accounts such as on the use of raw materials, water, energy or land, waste flows and emissions are combined with accounts on economic data such as gross domestic product or value added. The key advantage of environmental-economic accounting lies in the possibility to assess the impacts of economic activities on the environment and vice versa, i.e. assessing the impacts of environmental policies on socio-economic indicators.

Attempts by the UN to establish a common basis for global environmental accounting were set in 1993. Following several revisions and consultation processes, in 2012 the first international standard for environmental-economic accounting was adopted, and since 2014 the official version of the SEEA Central Framework is available. The UN system can be seen as an umbrella for the multiannual European strategy for environmental accounts (ESEA) as well as the EU regulation on European environmental accounts, which is implemented in all member states.

Environmental-economic accounts – the basics

Environmental-economic accounting captures environmental flows, stocks of environmental assets and economic activity related to the environment. The same methodological approach and classification is applied to environmental data as in the System of National Accounts (SNA). By that means the above-mentioned integration of environmental and economic information can be achieved. The concept follows a modular approach to enable national statistical offices to implement accounting gradually, taking into account national differences in methodology and data availability.

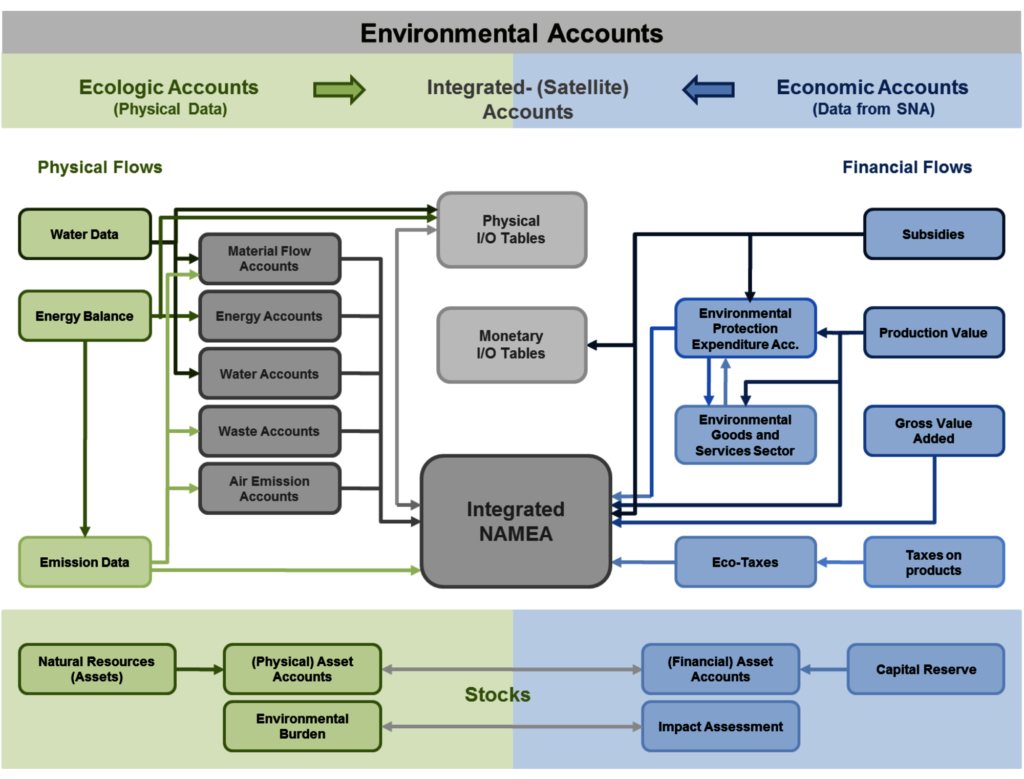

The following figure depicts the various components of environmental-economic accounts, depicted around the European accounting framework of the “Integrated National Accounting Matrix including Environmental Accounts (NAMEA)”.

(Environment Agency Austria, 2021)

The monetary accounts that are available through the regular national accounts are adjusted and disaggregated in certain areas. This includes particularly financial flows such as environmental and resource management expenditures, transfers that are associated with environmental impacts (e.g. environmentally relevant taxes), and the production of environmental goods and services. The physical accounts incorporate flows of natural resources through the economy. As flows always cause a change in stocks, these are also depicted as so-called “environmental assets”. However, achieving comprehensive accounts of natural assets is a very complex task.

For a series of natural resources or environmental pressures environmental accounts already exist, for some of which the SEEA provides specific sub-manuals. Among the first established accounts were the air emission accounts, due to the political need for data required to monitor climate targets in the Kyoto Protocol. Material Flow Accounts (MFA) and associated analyses as a part of the physical data can be considered another core element of the environmental-economic accounting framework, as they capture the overall physical size of an economy, thus relating to all other accounts. See our Methods section for more information on the methodology of MFA and the Relevance section to learn where MFA is used in political initiatives and processes.

Advancing accounting methodologies: MFA in Austria and around the globe

The concept of MFA has its roots in the work of Robert Ayres who in 1969 revived the framework of socio-economic metabolism (SEM), with a fundamental critique of economic theory and its focus on monetary flows. SEM stresses the dependence of economic processes on physical entities such as natural resources. MFA constitutes a practical realization of SEM that enables capturing the physical dimension of the economy. The first applications of modern MFA-research trace back 30 years, where research groups in Austria at the Institute for Social Ecology (SEC), in Germany at the Wuppertal Institute (WI) and in Japan at the National Institute for Environmental Studies (NIES) laid the groundwork for the modern accounting standards. In various multilateral research projects, as well as in statistical institutions such as the European Statistical Office (Eurostat) and international organisations such as the OECD, the methods and indicators were further developed, standardised, and extended. Today MFA provides fundamental environmental indicators informing policies, and a substantial branch of research applying MFA analyses has been established

One of the key MFA indicators, the material footprint, enables monitoring outsourcing of material-intensive stages of the supply chain and quantifying material demand of final consumption. Especially for SDG 8 and SDG 12 the material footprint is a core indicator. To ensure proper monitoring, data on material footprints need to be provided and to follow the same comparable calculation approach. Early initiatives by individual countries, e.g. Austria and Germany, and specific European research projects started first attempts to develop and implement footprint methodologies, mainly based upon environmentally-extended input-output analysis. Consequently, in Austria, Germany, and several other countries, footprint accounts are already in place for many years. In the light of the necessity for SDG-reporting, at both the European and the international level efforts are being made by Eurostat the UN International Resource Panel as well as the OECD to develop standards for harmonising footprint methodologies.

Providing and communicating environmental accounts

Environmental-economic accounts are compiled by national statistical offices and hence available via their websites. At the European level, the Eurostat database provides data on a series of environmental accounts, such as, for instance, on Material Flows and Resource Productivity. Other data sources such as the UN IRP Global Material Flows Database provide raw data for countries world-wide, which can be used to set up national material flow accounts.

Apart from the raw data, various platforms are available that provide visualisations and analyses based upon environmental-economic accounts. These include this very website www.materialflows.net where the data of the UN IRP Global Material Flows Database are made more easily accessible through various kinds of visualisations and the story section that sets relevant topics in context with the data. Another example is the Sustainable Consumption and Production Hotspot Analysis Tool (SCP-HAT), which allows to conduct analyses regarding the SCP performance of individual countries. In addition to material flows, also other environmental pressures and related impacts as well as socio-economic data can be set in context and analysed.

Environmental-economic accounting and MFA at its heart are powerful tools providing the empirical foundation for policies that aim at a more sustainable economy and way of living. Apart from the methodological standards, capacity building is needed to ensure that statisticians around the globe acquire the skills to compile physical accounts and policy designers have knowledge in interpreting the results. Ongoing processes at national, European and global levels aim at realising this necessary next step.

References

Environment Agency Austria, Environmental Accounting, 2021. URL https://www.umweltgesamtrechnung.at/en

Eurostat, 2021. Handbook for estimating raw material equivalents, of imports and exports and RME-based indicators on the country level – based on Eurostat’s EU RME model. URL https://ec.europa.eu/eurostat/documents/1798247/6874172/Handbook-country-RME-tool

Federal Statistical Office Germany, 2021. URL https://www.destatis.de/EN/Themes/Society-Environment/Environment/Environmental-Economic-Accounting/_node.html;jsessionid=65755AFD236B918AD2F8246949B5EF32.live742

Fischer-Kowalski, M., Krausmann, F., Giljum, S., Lutter, S., Mayer, A., Bringezu, S., Moriguchi, Y., Schütz, H., Schandl, H., Weisz, H., 2011. Methodology and Indicators of Economy-wide Material Flow Accounting. Journal of Industrial Ecololgy 15, 855–876. https://doi.org/10.1111/j.1530-9290.2011.00366.x

Krausmann, F., Weisz, H., Eisenmenger, N., 2018. Economy-wide material flow accounting: introduction and guide, Version 1.2., Social ecology working paper. Alpen-Adria Universität Klagenfurt, Wien, Graz, iff – Social Ecology Vienna, Vienna.

Ruijs, A., van der Heide, M., van den Berg, J., 2018. Natural Capital Accounting for the Sustainable Development Goals. Current and potential uses and steps forward. PBL Netherlands Environmental Assessment Agency, The Hague.

Statistics Austria, Material Flow Accounts, 2021. URL http://www.statistik.at/web_en/statistics/EnergyEnvironmentInnovationMobility/energy_environment/environment/material_flow_accounts_mfa/index.html

United Nations Environment Programme (UNEP), 2021. The use of natural resources in the economy, A Global Manual on Economy Wide Material Flow Accounting. URL https://www.resourcepanel.org/file/2330/download?token=AKG_oFKu

United Nations System of Environmental Accounting (SEEA), 2021. URL https://seea.un.org/content/seea-central-framework